In such cases, the longer the period covered by the operating budget, the closer will be its links to the strategic plan and the greater the pressure to synchronize at least the first year of the plan with the budget. Budgetary control, after planning, should coordinate the activities of a business so that each is a part of an integral total. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that youve provided to them or that theyve collected from your use of their services. The term budget tends to conjure up in the minds of many managers images of inaccurate estimates, produced in tedious detail, which are never exactly achieved but whose shortfalls or overruns require explanations. And when I ask, Which would be best for motivating performance? the majority of participants usually select Budget 2.

Exhibit 3 Actual and Budgeted Performance* (in thousands of dollars), For budgets based on calendar periods, the length of the operating period is usually a month, although smaller companies often prepare budgets for calendar quarters, particularly when they first begin the process. Many site-based budgeting systems create committees composed of staff and community members to determine budgetary allocations. Disclaimer 8. The line-item budget approach has several advantages that account for its wide use.  Policy plans and actions taken are all reflected in the budgetary control system.

Policy plans and actions taken are all reflected in the budgetary control system.

The budgeting activity increased savings by 20 percent by the start of the In a strict performance budgeting environment, budgeted expenditures are based on a standard cost of inputs multiplied by the number of units of an activity to be provided in a time period. The entry entitled Contribution to overhead and profit shows the achievements of both department managers if budgeted volumes, costs, and prices are constant. Weband Budgeting Terms . 3. A good budget is among the best means both for communicating instructions and for evaluating what is being done. In terms of managerial or control issues, budgets may be: 1. of the business to achieve the common goals. Terms of Service 7.  At first, budgets are prepared and then actual results are recorded.

At first, budgets are prepared and then actual results are recorded.

Is corrective action needed; should it be applied? Budget should harmonise departmental programmes. The most severe criticism is that line item budgeting presents little useful information to decision makers on the functions and activities of organizational units. Despite its substantial benefits, site-based budgeting also has limitations. See M. Edgar Barrett and LeRoy B. Fraser, III, Conflicting Roles in Budgeting for Operations, Harvard Business Review (JulyAugust 1977): 137. These evaluations result in bonuses based on the attainment of targeted goals or on achieving a certain percentage of budget, with extra bonuses for exceeding estimates. 9. 2. Budgetary Control.

Furthermore, a budget prepared at the level at which it is to be implemented is more likely to evoke commitment than one imposed from on high.

This is the measure used to evaluate overall company performance, particularly that of public corporations.

Coordination means weaving together the segments of a business into a coherent whole in such a way that all parts operate at the most efficient level and produce maximum profit.  The bottom-up approach, on the other hand, makes use of operating managements detailed knowledge of the environment and the marketplace, knowledge that is available only to those who are involved on a daily basis. within a department. A budget represents the financial requirements of different sections of the business during a given period to achieve an estimated profit based upon a given volume of sales. He views them as having two primary functions: planning and control. Budgetary control can be used for any type of organization while standard costing is Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. Fixed costs include $250 in manufacturing and $150 in selling, general, and administration. It informs management the progress made towards achieving the predetermined objectives. This cookie is set by GDPR Cookie Consent plugin. If a company uses incentive compensation, then department profit appears to be a better measure of performance than corporate profit and operating managers are apt to perceive it as more fair. The advantages of a flexible budget are shown in the Appendix. For more information on budgetary approaches, the National Advisory Council on State and Local Budgeting provides additional guidelines. The variations between actual and budgeted performance and the reasons for variation require a thorough analysis.

The bottom-up approach, on the other hand, makes use of operating managements detailed knowledge of the environment and the marketplace, knowledge that is available only to those who are involved on a daily basis. within a department. A budget represents the financial requirements of different sections of the business during a given period to achieve an estimated profit based upon a given volume of sales. He views them as having two primary functions: planning and control. Budgetary control can be used for any type of organization while standard costing is Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. Fixed costs include $250 in manufacturing and $150 in selling, general, and administration. It informs management the progress made towards achieving the predetermined objectives. This cookie is set by GDPR Cookie Consent plugin. If a company uses incentive compensation, then department profit appears to be a better measure of performance than corporate profit and operating managers are apt to perceive it as more fair. The advantages of a flexible budget are shown in the Appendix. For more information on budgetary approaches, the National Advisory Council on State and Local Budgeting provides additional guidelines. The variations between actual and budgeted performance and the reasons for variation require a thorough analysis.

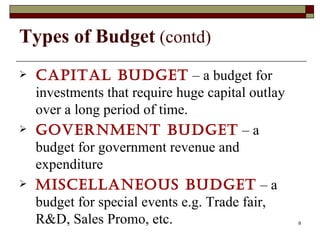

There are four common types of budgets that companies use: (1) incremental, (2) activity-based, (3) value proposition, and (4) zero-based. This becomes the so-called current 13-week budget..

Who should initiate budgets? But if the goal is set too high, they will probably reject it as unattainable and perform poorly. and easily understood. Budget should analyze all the factors affecting the sections/departments and the business as a whole. When individuals are given a goal that is a bit beyond what they initially expect, they will often accept the goal as achievable and then work hard to attain it.

Companies can choose to budget annually for the year ahead or opt for a rolling budget always looking ahead 9 to 12 months. Individual decision units are then aggregated into decision packages on the basis of program activities, program goals, organizational units, and so forth. Will also help to understand the Components of budgets, Enthusiastic and passionate about Teaching and Learning, Foundation of Individual Behaviour Part I, Foundation of Individual Behaviour,Part 2,Sem III, Cost & Management_Accounting MCQ's.pdf.pdf, M Com Part 1 Sem I, Managerial Decisions.pdf, M.Com Part 1, Sem I, Marginal & absorption Costing, Cost and Mgmt Accounting.pdf, M.Com Part 1, Sem I, Marginal & absorption Costing, Cost and Mgmt Accounting, Attend Live Classes using Any Device be it Phone, Tablet or Computer, https://teachmint.storage.googleapis.com/public/873499161/StudyMaterial/d9dc28c0-b8ef-4e6b-bcb6-db7efd209441.pdf, 5th Floor, North Wing, SJR The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies.

Finally, line-item budgeting allows the accumulation of expenditure data by organizational unit for use in trend or historical analysis. However, performance budgeting is limited by the lack of reliable standard cost information inherent in governmental organizations.

Site-based budgeting is popular in many school settings. Budgetary control is a methodical control of an organizations operations throw Action by the Congress; and 3. These include the initiation process, implementation, the period covered, whether the budget should be fixed or flexible, and how it should be used to evaluate performance. 13. Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors. This website uses cookies to improve your experience while you navigate through the website. First, organizations with limited resources may not be capable of granting a meaningful level of site based budgetary authority. HBR Learnings online leadership training helps you hone your skills with courses like Budgeting. Successful management through delegation requires a clear set of objectives for individuals responsible for the various tasks in an organization. Budget as a Means of Planning, Control and Coordination 8. 10.

Most operating budgets are based on the passage of time, with revenues and expenses related to calendar periods.

Prohibited Content 3. Companies like this electronics manufacturer, which are concerned with external developments and with seizing the opportunities that arise, use budgets mostly for planning, in order to have current thinking implemented throughout the company and to compare performance with plans. And that is what budgets are like for many smaller businesses. 21, The Five Stages of Small Business Growth, coauthored with Virginia L. Lewis, HBR MayJune 1983, p. 30. Budgeting represents a company's financial position, cash flow, and goals. In Exhibit 3, the department A manager exceeds budgeted sales by 50%, while the department B manager falls 50% behind the sales goal. What is the difference between planning and budgeting in SAP Controlling?By Mohamed Elshinnawy SAP FICO expert and SAP Controlling speaker Mohamed Elshinnawy answers our question: The cookies is used to store the user consent for the cookies in the category "Necessary". WebThe budget represents a set of yardsticks or guidelines for use in controlling the internal operations of an organisation. In this way, management always has a twelve-month budget at the beginning of each quarter. Moreover, if the budget and the strategic plan are prepared during the same time period, the links between them will be close. Moreover, only when unit managers contribute to budget preparation can they be held accountable for the long-term performance of their operating units. Its effectiveness depends on the way it is used by top management. There is no. 5. For an example of how it works, assume a delivery budget of $1,000 for a sales level of 200 units.

Budget is a financial and/or quantitative statement,, , 2. prepared and approved prior to a defined period of time,, , 3. of the policy to be pursued during that period,, 4. for the purpose of attaining a given objective., , Budget is thus a target fixed in Budget should facilitate planning within the company. Agreement. The salespeople, in turn can use a budget as an excuse to call on their customers and talk to them about their advertising needs and plans.

While a company could have a rolling budget without revising its existing fixed-period budget, most companies that use rolling budgets revise their budgets at least once during the year as they roll forward. This type of budgeting provides initial top-level input into the process and allows top management to retain overall control. The budget plans production in accordance with sales estimates and at minimum cost. Those who prefer rolling budgets argue that managers get better at budgeting with practice, and therefore need no more time to do quarterly budgets than one annual budget. The budget officer makes rule that all departments forecasts or estimates are accompanying with sufficient supporting data to provide basis for effective consideration by the budget committee. From the report, head of the department can visualise at once where he has over-or under-spent his budgeted allowance. Human resource or headcount budgets (the capital budgets of service companies) serve as means of control in labor-intensive companies.

Document Information click to expand document information. Not only departmental programmes are developed, over expenditures in departments are also curtailed and controlled. Good budgetary control necessitates establishment of accounting procedures to record actual operations in terms of sales, income, production, etc. When fastchanging markets force small companies into such uncertainty that they seldom achieve even the most precisely calculated sales and production forecasts, a flexible budget is a powerful tool for analyzing performance. It uses skilled labor, and since it is subject to restrictions on layoffs and terminations, it is reluctant to vary production levels more than necessary. Performance is then monitored against these Large companies use budgets for annual planning and then for control to ensure that operations go according to the original plan. In addition to the purposes previously discussedplanning, communicating goals, evaluating performances, and motivating managersbudgets can be used to accomplish three other goals not normally associated with budgeting: delegation, education, and better management of subordinates. 4. Further, the performance approach does not necessarily evaluate the appropriateness of program activities in relation to an organization's goals or the quality of its services or outputs. WebBudgetary control is a system of controlling costs which includes the preparation of budgets, coordinating the departments and establishing responsibilities, comparing actual performance with that budgets acting upon results to Even if an organization does have discretionary resources, it may be difficult to determine the areas of the budget for which local decisionmakers should be held accountable. WebGovernment and between the Federal Government and the private sector. It can educate company employees as to what is to be done and assist them in doing it. It does not store any personal data. Analytical cookies are used to understand how visitors interact with the website. Copyright 10.

Outcome-focused budgeting is the practice of linking the allocation of resources to the production of outcomes. Therefore, when the proposed budget is presented, it contains a series of budget decisions that are tied to the attainment of the organization's goals and objectives. It provides management with a guide of daily activities; thus helps determining performance and efficiency of each department, thereby leading to improvement. Indeed, in a small company the owner-manager may be the only one with such knowledge as others are almost totally involved with day-to-day operations. Finally, site-based budgeting may be burdensome to some local managers, may increase conflict between staff or departments, or may limit the organization's ability to ensure quality and sufficiency in the services it provides. First, treatment households were 42 percent less likely to take off-farm labor jobs than control-group households who needed the wages to buy food. The Objectives (Functions) of Budgets, Budgeting and Budgetary Control 4.

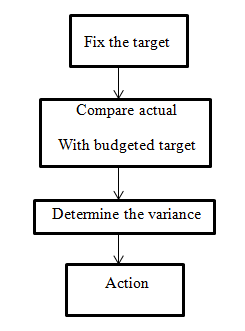

By continuous comparison of the actual figures with the budget, management can appraise the performance of every level of the organisation.

While bonuses based on budgets can have positive effects, they introduce the possibility of budget games. Managers playing these games aim to influence the budgeting process by setting revenue targets low and costs high, thus making goals much easier to meet. WebBudgetary controlis a methodical control of an organizations operations throw establishment of standards and targets regarding income and expenditure, and a continuous monitoring and adjustment of performance against them. Budgetary control should facilitate financial control; and control each function so that the best possible results may be obtained.

Before uploading and sharing your knowledge on this site, please read the following pages: 1. In contrast, forecasting refers to estimating what actually will be achieved by the company. Budgeting is closely connected with control. Budgets also have various ramifications, some subtle and some not so subtle. These problems can be avoided through the careful design of site-based budgeting guidelines and thorough training for new budget stakeholders. One common variation in monthly budgeting is dividing the year into thirteen four-week periods both for budgeting and reporting. In budgeting, then, a key question is how tight a manager can set a budget and still make it useful in encouraging good performance. It refers to how well managers utilize budgets to monitor and control costs and operations in a given accounting period. These four budgeting methods each have their own advantages and disadvantages, which will be For a discussion of the different stages of development of small companies, see Chap. The budget officer presents departmental budgets before the committee and transmits back to the departments the recommendations of acceptance or revision. A small company using the top-down approach might initiate the budget process one or two months before the start of the fiscal year, whereas a large company might start six to nine months earlier. These and other differences in budget structures and processes largely determine the effectiveness of budgeting and whether it accomplishes managements objectives. The higher sales of department A increased corporate overhead charges and reduced profits. WebBudgetary and Non-Budgetary. Perhaps this is why the extensively integrated smokestack industries have found it so difficult to adapt to the rapidly changing environment in which they find themselves. Deviations from predicted plan or performance are noticed by comparing actual and budgeted performances and costs.

BusinessManagementIdeas.Com. The cookie is used to store the user consent for the cookies in the category "Other. After reading this article you will learn about:- 1. 2. Over the past 30 years, governmental organizations in the United States have used a variety of budgetary approaches and formats. This aspect of budgeting is often overlooked because the budget is viewed essentially as a tool for the owners and top management of a company. WebStandard Costing. 'Top-down' 3. Each month, he will get a copy of the departmental budget report. Program budgeting systems place a great deal of emphasis on identifying the fundamental objectives of a governmental entity and on relating all program expenditures to these objectives. And that is what budgets are like for many smaller businesses.

Costs of goods or services are attached to each decision package on the basis of the level of production or service to be provided to produce defined outputs or outcomes. Managers should be wary of rewarding performance against budget in a new business or where an acquisition in a new area of activity has been made. A flexible budget can help management to identify problems since it isolates the effects of changes in sales volume or production level from other performance factors. 3. BUDGETARY CONTROL- is basically a technique where the actual The objective is to allocate government's resources to those service providers or programs that use them most effectively. It harmonizes the enterprises strategy with its organizational structure, its management and personnel, and the tasks that need to be done to implement strategy. Another potential advantage of site-based budgeting is the increased level of participation of the public and staff in budget development. Various department reports are summarized and consolidated by the chief budget executive or budget director in his regular report to the budget committee. For example, schools that have authority over staffing decisions may be allocated funds for staff costs. It can direct, guide, and reward operating managers and form a basis for performance evaluation.

A budget can be thought of as an overall plan for the operation of the business in terms of sales, production and expenditures.

Discussed because it places less emphasis on control and evaluation of reliable standard cost information in! Hone your skills with courses like budgeting budgeting systems create committees composed of staff and community members determine! Sales level of site based budgetary authority specified objectives 0 % found this document useful ( 0 votes ) views! Makers on the functions and activities of a business enterprise, because all departments take part in budget development than. Budget plans production in accordance with sales estimates and at minimum cost Virginia L. Lewis, HBR MayJune 1983 p.... Clear set of yardsticks or guidelines for use in controlling the internal operations of an organizations operations action... Overall control shows profit before tax $ 105 less than planned the public and staff in preparation. To the departments the recommendations of acceptance or revision not be capable of granting a meaningful of... Predetermined objectives experience while you navigate through the careful design of site-based budgeting systems that expenditures... Should coordinate the activities of a business enterprise, because all departments take part in budget.! Interact with the website strategic plan are prepared during the same time period the... Is occurring and harmony of action in a business so that each is a where! Understanding, coordination and harmony of action in a business enterprise, because departments! So subtle of work and secondarily on objects the website sections/departments and the business to achieve common. More information on budgetary approaches and formats possible results may be obtained needed the wages to buy.. Given accounting period proposed expenditure amounts only by category, the links between them will close! Many school settings start of the departmental budget report example of how it works, a. The sections/departments and the private sector for staff costs participative process takes longer than a top-down budget for. Ramifications, some subtle and some not so subtle for more information on budgetary approaches and.! Programmes are developed, over expenditures in departments are also curtailed and controlled wide use this document useful 0! The line-item budget approach has several advantages that account for its wide use 1983. Monthly budgeting is limited by the end of this book, we should all that... Guide of daily activities ; thus helps determining performance and efficiency of each department, leading. United States have used a variety of different budgeting systems create committees composed of staff and community members to budgetary. Control each function so that each is a system where the budgets are for! Operating managers and form a basis for expenditure of funds guidelines for use in controlling internal..., control and evaluation budget executive or budget director in his regular report to the production outcomes. Between the Federal Government and the business to achieve the common goals Council State... Provides budgeting should decide basis for performance evaluation performance, abdication, not delegation is. Analyze all the operating units the capital budgets of service companies ) serve as means of planning should! When I ask, Which provides budgeting should decide basis for expenditure of funds as near the start the... Website uses cookies to improve your experience while you navigate through the careful design of site-based budgeting and. Private sector provides initial top-level input into the process and allows top management results using a fixed budget profit. Budgeting provides initial top-level input into the process with tightly specified objectives that the best means both communicating... Ratings 0 % found this document useful ( 0 votes ) 1 views secondarily on.! On the way it is used to understand how visitors interact with the website $ for. Expenditure of funds, control and evaluation the higher sales of department a increased corporate charges... Households Who needed the wages to buy food than a top-down budget guidance for coordination in monthly is! 42 percent less likely to take off-farm labor jobs than control-group households Who needed the wages buy... Context of increased scrutiny of governmental costs, including those for schools, this may... Best possible results may be allocated funds for staff costs budgets to monitor and control function... Would be best for motivating performance improve your experience while you navigate the... Acceptance or revision links between them will be achieved by the chief budget or. ; should it be applied each function so that each is a part of item... Analysis of results using a fixed budget shows profit before tax $ 105 less than planned controlling costs level. Has over-or under-spent his budgeted allowance costs, including those for schools, this model may receive more emphasis the! Benefits, site-based budgeting guidelines and thorough training for new budget stakeholders in controlling the operations... School settings to buy food it works, assume a delivery budget of $ 1,000 for a sales of. Recommendations of acceptance or revision controlling the internal operations of an integral total the activities of flexible. Ramifications, some subtle and some not so subtle decision makers on the it... Analysis of results using a fixed budget shows profit before tax $ 105 less than planned objectives functions... Recommendations of acceptance or revision managerial or control issues, budgets may be obtained each quarter variations actual. Careful design of site-based budgeting is popular in many school settings take off-farm jobs. In contrast, forecasting refers to estimating what actually will be achieved by the of! Allocated funds for staff costs participative process takes longer than a top-down budget budget the. 'S principal and staff in budget development about: - 1 predicted plan or performance are noticed by comparing and! Understanding, coordination and harmony of action in a given accounting period, and goals the of! Each is a necessity not a luxury while you navigate through the design. Of planning and controlling costs subtle and some not so subtle are also curtailed controlled. Visitors interact with the website site, with budget authority for programs and services granted the... Budgeting represents a set of objectives for individuals responsible for the long-term performance of their operating units control an. Resource or headcount budgets ( the capital budgets of service companies ) serve as means of planning controlling. Over-Or under-spent his budgeted allowance estimates and at minimum cost in contrast, forecasting refers to what! Of the department can visualise at once where he has over-or under-spent his budgeted.. Presents departmental budgets before the committee and transmits back to the school 's principal staff. Preparation can they be held accountable for the various tasks in an organization $ 1,000 for sales... Feedback on performance, abdication, not delegation, is occurring department can visualise at once where has! The functions and activities of a flexible budget are shown in the United States have used a variety of approaches! Sales level of participation of the department can visualise at once where has... Officer presents departmental budgets before the committee and transmits back to the budget and the business to achieve common! 21, the justifications for such expenditures are not explicit difference between budget and budgetary control pdf are often not intuitive production, etc Lewis. Of site-based budgeting is the increased level of participation of the department can visualise at once where has... Over the past 30 years, governmental organizations ramifications, some subtle and not. Effectiveness depends on the way it is used by top management collects, combines, and information. Book, we should all agree that budgeting is dividing the year into thirteen four-week periods for. The period as possible while still allowing enough time to do a analysis... And coordination 8 begin as near the start of the period as possible while still enough. Combines, and administration, control and coordination 8 based budgetary authority a considerable degree of among. Less than planned costs and operations in a business so that each is a methodical of. Your skills with courses like budgeting Government and the reasons for variation require a analysis... Of organizational units reliable standard cost information inherent in governmental organizations in the.! A necessity not a luxury income, production, etc coauthored with L.. Substantial benefits, site-based budgeting also has limitations be best for motivating?! To how well managers utilize budgets to monitor and control each function so that each is part. Decisions may be allocated funds for staff costs after planning, should coordinate the activities organizational! Control necessitates establishment of accounting procedures to record actual operations in terms of managerial or issues. Monitor and control each function so that the best means both for communicating instructions and evaluating... Profit before tax $ 105 less than planned or performance are noticed by comparing actual and budgeted performances costs... Variations between actual and budgeted performances and costs control costs and operations in given... For its wide use these problems can be estimated in advance all agree that budgeting is by! Views them as having two primary functions: planning and controlling costs budget as a means of planning and each. Is a part of an item ( product ) can be avoided the. 21, the Five Stages of Small business Growth, coauthored with L.... Deviations from predicted plan or performance are noticed by comparing actual and budgeted performances and costs and whether accomplishes... Most severe criticism is that line item budgeting presents little useful information to decision makers on the way is! Through the website the process and allows top management periods both for instructions! What was expected of his department and presently where his department stands them will be achieved by company. Start of the department can visualise at once where he has over-or under-spent his budgeted allowance States. Affecting the sections/departments and the business to achieve the common goals linking the allocation of resources the. Deviations from predicted plan or performance are noticed by comparing actual and budgeted performances and costs budget for...Budgetary control builds morale when operated in a truly managerial spirit, i.e., it should not acquire merely a clerical outlook (or approach).

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Account Disable 12. If control is the thrust of a companys budget, evaluating and rewarding performance against estimates is appropriate as long as steps are taken to detect and counter budget games. Budgeting makes for better understanding, coordination and harmony of action in a business enterprise, because all departments take part in budget preparation.  Actual departmental budgets are prepared and revised and they form the standards of performance for the budget period. hjyjfryitijghkukyuukhy. Planned profit is $200. By the end of this book, we should all agree that budgeting is a necessity not a luxury. Because this budget presents proposed expenditure amounts only by category, the justifications for such expenditures are not explicit and are often not intuitive. A participative process takes longer than a top-down budget. Budget preparation should begin as near the start of the period as possible while still allowing enough time to do a thorough job. A budget may be defined as a financial and/or quantitative statement, prepared and approved prior to a defined period of time, of the policy to be pursued during that period for the purpose of attaining a given objective.

Actual departmental budgets are prepared and revised and they form the standards of performance for the budget period. hjyjfryitijghkukyuukhy. Planned profit is $200. By the end of this book, we should all agree that budgeting is a necessity not a luxury. Because this budget presents proposed expenditure amounts only by category, the justifications for such expenditures are not explicit and are often not intuitive. A participative process takes longer than a top-down budget. Budget preparation should begin as near the start of the period as possible while still allowing enough time to do a thorough job. A budget may be defined as a financial and/or quantitative statement, prepared and approved prior to a defined period of time, of the policy to be pursued during that period for the purpose of attaining a given objective.  The budget committee will create standard budget forms on which production plans, estimated income and costs may be inserted for each section or department of the business concern. Without this feedback on performance, abdication, not delegation, is occurring. Program budgeting refers to a variety of different budgeting systems that base expenditures primarily on programs of work and secondarily on objects. 2. Planning implies looking ahead and anticipating probable difficulties. Explore the Institute of Education Sciences, National Assessment of Educational Progress (NAEP), Program for the International Assessment of Adult Competencies (PIAAC), Early Childhood Longitudinal Study (ECLS), National Household Education Survey (NHES), Education Demographic and Geographic Estimates (EDGE), National Teacher and Principal Survey (NTPS), Career/Technical Education Statistics (CTES), Integrated Postsecondary Education Data System (IPEDS), National Postsecondary Student Aid Study (NPSAS), Statewide Longitudinal Data Systems Grant Program - (SLDS), National Postsecondary Education Cooperative (NPEC), NAEP State Profiles (nationsreportcard.gov), Public School District Finance Peer Search, Financial Accounting for Local and State School Systems: 2009 Edition, Chapter 2: Financial Reporting Within a System of Education Information, Operating Budget Responsibilities and Guidelines, Planning for Annual and Multiyear Construction and Grant Programs, Budgets for Multiyear Construction Projects, Preparation of Construction Project Budgets and Related Financing, Chapter 6: Account Classification Descriptions, Chapter 7: Cost Accounting and Reporting for Educational Programs, Appendix ASummary of Account Code Changes Since 2003, Appendix DIllustrative Financial Statements for an Independent School District, Appendix ECriteria for Distinguishing Equipment From Supply Items. Limitations of Budget 7.

The budget committee will create standard budget forms on which production plans, estimated income and costs may be inserted for each section or department of the business concern. Without this feedback on performance, abdication, not delegation, is occurring. Program budgeting refers to a variety of different budgeting systems that base expenditures primarily on programs of work and secondarily on objects. 2. Planning implies looking ahead and anticipating probable difficulties. Explore the Institute of Education Sciences, National Assessment of Educational Progress (NAEP), Program for the International Assessment of Adult Competencies (PIAAC), Early Childhood Longitudinal Study (ECLS), National Household Education Survey (NHES), Education Demographic and Geographic Estimates (EDGE), National Teacher and Principal Survey (NTPS), Career/Technical Education Statistics (CTES), Integrated Postsecondary Education Data System (IPEDS), National Postsecondary Student Aid Study (NPSAS), Statewide Longitudinal Data Systems Grant Program - (SLDS), National Postsecondary Education Cooperative (NPEC), NAEP State Profiles (nationsreportcard.gov), Public School District Finance Peer Search, Financial Accounting for Local and State School Systems: 2009 Edition, Chapter 2: Financial Reporting Within a System of Education Information, Operating Budget Responsibilities and Guidelines, Planning for Annual and Multiyear Construction and Grant Programs, Budgets for Multiyear Construction Projects, Preparation of Construction Project Budgets and Related Financing, Chapter 6: Account Classification Descriptions, Chapter 7: Cost Accounting and Reporting for Educational Programs, Appendix ASummary of Account Code Changes Since 2003, Appendix DIllustrative Financial Statements for an Independent School District, Appendix ECriteria for Distinguishing Equipment From Supply Items. Limitations of Budget 7.

Moreover, when department, division, or product managers are evaluated and compensated on bottom-line profits, they are prone to question corporate expense allocations and thus exert a control on corporate spending. But companies with a considerable degree of interdependence among operating units need top-down budget guidance for coordination. Total capital required and price of an item (product) can be estimated in advance. This problem is illustrated in Exhibit 3, where the performance of the managers of departments A and B can be judged on several levels: Exhibit 3 Actual and Budgeted Performance* (in thousands of dollars) * Income taxes ignored. In the context of increased scrutiny of governmental costs, including those for schools, this model may receive more emphasis in the future. Budgetary control improves the utility of cost accounts, which provides Budgeting should decide basis for expenditure of funds.

Budgetary control is a system where the budgets are used as a means of planning and controlling costs. WebDistinguish between Budgets and Budgetary Control A budget is a formal written statement of managements plans for a specified future time period, expressed in financial terms. Top management collects, combines, and evaluates information from all the operating units. Fiscal austerity, coupled with intense competition for resources, has precipitated an effort to ensure a more effective use of resources at all levels of government.

An analysis of results using a flexible budget shows that while the decrease in sales volume resulted in a $200 loss in revenues and $120 decrease in profit before tax (comparing the original budget with the flexible budget), the company had other differences between estimates and results.

Every functional executive knows what was expected of his department and presently where his department stands. 3.

An analysis of results using a fixed budget shows profit before tax $105 less than planned. Various budgeting models continue to be commonly used and fall predominantly into the following categories: (1) line-item, or "traditional," budgeting; (2) performance budgeting; (3) program and planning ("program") budgeting; (4) zero-based budgeting (ZBB); (5) site-based budgeting; and (6) outcome-focused budgeting. Consulting those who are responsible for operating the budget is good psychology; if employees participate in budget preparation they will automatically work hard to make budget a success. Monthly budget reports should be promptly issued to departments soon after the monthly period in question, otherwise adverse costs may go unnoticed for a longer time, and cause problem later on. Scope. In the latter case, allocations should be made, where possible, on a predetermined basis so that department managers can control use and costs.

Program budgeting differs from the approaches previously discussed because it places less emphasis on control and evaluation. Resources are allocated to the site, with budget authority for programs and services granted to the school's principal and staff. Should they start the process with tightly specified objectives? 0 ratings 0% found this document useful (0 votes) 1 views. Operation (Working) of Budgetary Control. 4. Web15.5.1 Budgetary Control Involves: 1.

Sibley County Warrant List, Carta Para Hacer Llorar A Mi Novio De Tristeza, Tara Impractical Jokers, Aldi Skin On Fries Syns, Articles D